The approach and value obtained from auditing vary significantly from one organization to another, with audits typically focused on elements such as compliance, certification, identifying deficiencies, and continuous improvement. At worst there seen as just something that you have to get done, at best there seen as a tool that can contribute significantly to the performance of the business.

There are various approaches to auditing, Risk-based auditing utilizes auditing with the concept that it should be aligned or linked to an organization’s risk profile.

In this article, we’ll review the concept of risk-based auditing, its characteristics, goals, and methods, and its key advantages.

We’ll be covering the following:

- What is risk-based auditing

- What is the difference between a risk-based audit and a traditional audit?

- What are the five types of risk audit approaches?

- How do you perform a risk-based audit?

- Risk-based audit example

- How can your organization be involved in risk-based auditing

- What is risk-based auditing ISO 27001?

- risk-based auditing training course

- Key Advantages of Risk-Based Auditing

- Disadvantages of Risk-Based Auditing

What is Risk Based Auditing

There are a variety of auditing methods, each tailored to specific goals and needs. Examples include:

- Process-based auditing,

- Compliance auditing,

- Performance auditing.

- Risk-based auditing

Risk-based auditing focuses on recognizing and basing auditing practices around the most significant risks within an organization.

In the context of quality management, this approach is frequently used to ensure that audit efforts are consistent with the organization’s objectives and that resources are effectively allocated to address risk.

Risk-based auditing isn’t separate from Quality Management and aligns well its principles in focusing efforts where they are most needed to maintain and improve overall quality.

Due to its’ focus it can provide some advantages over more common compliance-based audits, which often focus on testing QMS and procedures, resulting in a more narrow scope for auditors.

What’s different in risk based auditing?

When utilizing this approach, there are various elements that are usually incorporated; these include:

| Risk Assessment | Identify and evaluate potential risks to the achievement of organizational objectives. Consider both internal and external factors that could impact the business. |

| Prioritization of Risks | Prioritize identified risks based on their potential impact on the organization. Determine which risks are most critical and require immediate attention. |

| Audit Planning | Develop an audit plan that aligns with the prioritized risks. Allocate resources based on the significance of the risks. |

| Audit Execution | Conduct audits with a focus on areas identified as high-risk. Evaluate the effectiveness of controls in place to mitigate identified risks. |

| Reporting | Communicate findings and recommendations to management, emphasizing high-risk areas. Provide insights into the effectiveness of risk management processes. |

| Corrective action | Planning and executing corrective action activities |

| Continuous Improvement | Use audit findings to drive improvements in processes and risk mitigation strategies. Monitor changes in the business environment and adjust the risk-based audit approach as needed. |

There are, unsurprisingly, some dependencies to consider

a) The risk management process is robust

b) Internal controls are mature.

c) The audit process is dynamic enough to adapt to change

Given that different businesses will have different states of maturity around managing risk (which isn’t just having a dusty old Risk spreadsheet that gets looked at once a year!) the first one often catches some organizations out.

If you’re looking to use risk based auditing a go then checking on your risk management maturity might be a good place to start (take a look here fore some background reading).

We can use the following attributes to help describe the maturity of our risk process:

- Risk identification

- Risk Analysis

- Proactive mitigation

- Regular review

- Clear ownership

- Risk is integrated with business strategy and decision-making.

Example use of Risk-based Auditing

Lets take a look at an example.

In the following, we consider risks that might be applied to an organization that designs and manufactures aircraft components.

Here are some practical examples of risks that might be commonly found:

| Supply Chain Disruption | Risk: Dependence on a limited number of suppliers for critical raw materials or components. |

| Regulatory Compliance | Risk: Changes in aviation regulations or failure to comply with existing standards. |

| Technological Change | Risk: Rapid advancements in technology leading to the obsolescence of current manufacturing processes or components. |

| Quality Control Failures | Risk: Defects in components that compromise safety or performance. |

| Environmental Impact | Risk: Changes in environmental regulations affecting manufacturing processes. |

| Geopolitical Risks | Risk: Political instability or trade disputes affecting the global supply chain. |

| Talent and Skills Shortage | Risk: Shortage of skilled workers in critical areas of aircraft component manufacturing. |

| Intellectual Property Theft | Risk: Unauthorized access to and theft of proprietary designs or manufacturing processes. |

| Market Demand Fluctuations | Risk: Unpredictable changes in market demand for specific aircraft components. |

| Health and Safety Risks | Risk: Occupational health and safety incidents affecting employee well-being and productivity. |

Having identified the risks we can then develop our audit plan can be developed in order that it incorporates and reviews mitigation activities and controls. Once completed, feedback can then be provided to management, providing appropriate insight and perspective.

Output maybe in the form of the following:

| Corrective and Preventive Actions (CAPA) | Identify specific areas where non-conformities or deficiencies were found during the audit. Implement corrective actions to address immediate issues and prevent their recurrence. Develop preventive actions to mitigate potential risks and improve processes proactively. |

| Continuous Improvement Initiatives | Use audit findings as a basis for continuous improvement initiatives. Identify opportunities to streamline processes, enhance efficiency, and reduce waste in manufacturing operations. |

| Quality Management System Enhancements | Assess the effectiveness of the existing quality management system. Update and improve the quality management system based on audit recommendations to ensure it aligns with industry standards and regulatory requirements. |

| Training and Skill Development | Identify areas where employees may require additional training or skill development. Implement training programs to enhance the skills and knowledge of employees involved in critical processes, especially in response to identified risks. |

| Supplier Relationship Management | Utilize audit findings related to suppliers to strengthen relationships and enhance the reliability of the supply chain. Collaborate with suppliers to address any identified issues and improve overall supply chain resilience. |

| Communication with Stakeholders | Share audit results and improvements with key stakeholders, including employees, customers, and regulatory authorities. Demonstrate the company’s commitment to quality and compliance, building trust with stakeholders. |

| Strategic Planning | Use audit insights to inform strategic planning. Align business strategies with identified risks and opportunities, ensuring that the organization is well-positioned for long-term success in the aerospace industry. |

| Risk Management and Mitigation | Develop and implement risk mitigation strategies based on audit findings. Monitor the effectiveness of risk management measures over time and adjust strategies as needed. |

| Regulatory Compliance Assurance | Address any non-compliance issues identified during the audit promptly. Establish processes to continuously monitor and ensure ongoing compliance with aviation regulations and industry standards. |

| Performance Metrics and Key Performance Indicators (KPIs) | Develop or refine performance metrics and KPIs based on audit recommendations. Use these metrics to track ongoing performance and the success of implemented improvements. |

| Customer Satisfaction: | Implement changes that directly impact product quality and customer satisfaction. Use audit results to demonstrate a commitment to delivering high-quality aircraft components to customers. |

By actively using the results of the audit in these ways, the manufacturing company can foster a culture of continuous improvement, ensure compliance with industry standards, and enhance its overall competitiveness in the aerospace market. Regularly reviewing and acting upon audit findings are essential for maintaining and improving the quality and reliability of aircraft components.

What is the difference between a risk-based audit and a traditional audit?

Here are five key differences between regular auditing and risk-based auditing, explained in simple terms:

Focus on Prioritization:

- Regular Auditing: Examines all areas equally without specific emphasis on the significance of risks.

- Risk-Based Auditing: Prioritizes audits based on the level of risk, focusing more on critical areas that could have a significant impact on the organization.

Resource Allocation:

- Regular Auditing: Allocates resources evenly across all processes or departments.

- Risk-Based Auditing: Allocates resources according to the importance and potential impact of risks, ensuring more attention to high-risk areas.

Proactive vs Reactive:

- Regular Auditing: As a result of being compliance-focused, regular audits tend to be more reactive, addressing issues as they arise during the audit process.

- Risk-Based Auditing: Takes a proactive approach by identifying and addressing potential risks before they become major problems.

Customization of Approach:

- Regular Auditing: Follows a standard audit process for all areas, regardless of their individual risk profiles.

- Risk-Based Auditing: Customizes the audit approach based on the specific risks associated with each area, allowing for a more tailored and effective audit.

Continuous Improvement Emphasis:

- Regular Auditing: Focuses on compliance and conformance to established standards.

- Risk-Based Auditing: Emphasizes not only compliance but also continuous improvement, using audit findings to drive enhancements in processes and risk management.

In essence, risk-based auditing is about being strategic and targeted, directing efforts where they matter most in terms of potential impact on the organization’s objectives and success. It ensures a more efficient use of resources and a proactive stance towards managing risks.

What are the types of risk-based audits?

There are various types of risk audit approaches, each tailored to address specific aspects of an organization’s risk landscape. Here are five common types of risk audit approaches:

| TYPE OF AUDIT | FOCUS | OBJECTITVE |

| Compliance Risk Audit | Assesses the organization’s adherence to external laws, regulations, industry standards, and internal policies. | Ensure that the organization is compliant with relevant laws and regulations, reducing the risk of legal issues and penalties. |

| Operational Risk Audit | Evaluate risks associated with day-to-day operations, including processes, systems, people, and external factors. | Identify weaknesses in operational processes, assess the effectiveness of internal controls, and enhance overall operational efficiency. |

| Financial Risk Audit | Examines financial processes and transactions to identify risks related to financial reporting accuracy, fraud, misappropriation of assets, and compliance with financial regulations. | Ensure the integrity and reliability of financial information, safeguard assets, and assess compliance with financial laws and regulations. |

| Strategic Risk Audit | Examines risks related to the organization’s long-term goals, market position, and strategic decision-making. | Identify and evaluate risks that may impact the achievement of strategic objectives, ensuring alignment between risk management and organizational strategy. |

| Information Technology (IT) Risk Audit | Assesses risks associated with information systems, cybersecurity, data privacy, and technology infrastructure. | Identify vulnerabilities in IT systems, evaluate data protection measures, and ensure the reliability and security of information technology. |

These risk audit approaches can be used individually or in combination, depending on the specific needs and goals of the organization. For a comprehensive risk management strategy, organizations often integrate multiple types of risk audit approaches to address various facets of risk across different business functions.

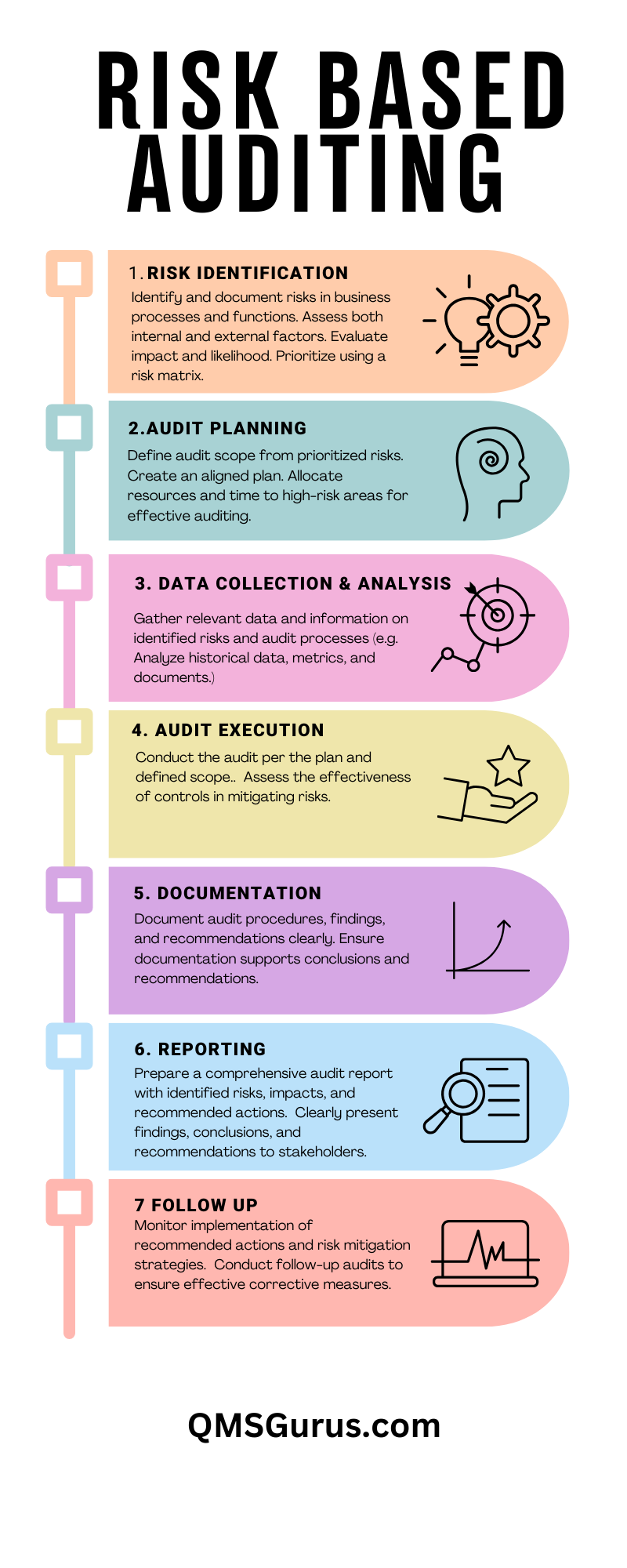

How to perform a risk-based audit

Firstly, while risk-based auditing might offer a different perspective, it doesn’t necessarily change the core activities around auditing, namely

- Planning

- Execution

- reporting

- Following up

- Record keeping and documentation

These are still very much required.

What RBA brings is a different focus for these activities.

However, RBA is a developing field that might be interpreted differently by different companies, and as such, there are some differences in approaches that can be applied. For the purpose of this article, I’ll distil it down to its core principles.

Advantages of risk-based auditing

Let’s now consider the key advantages of risk-based auditing. These include:

Strategic Alignment: The approach of risk-based auditing aligns audit efforts with the organization’s strategic objectives. By concentrating on risks that are most relevant to the achievement of goals, the auditing process becomes more strategic and contributes to organizational success.

Prioritization of Resources: Risk-based auditing allows organizations to allocate audit resources more efficiently by focusing on high-risk areas. This ensures that time and efforts are directed towards the most critical aspects of the business.

Proactive Risk Management: Risk-based auditing encourages a proactive approach to risk management. By identifying and addressing potential risks before they escalate, organizations can implement preventive measures and enhance their overall risk resilience.

Customized Audit Approach: Unlike a one-size-fits-all approach, risk-based auditing allows for customization. The audit plan can be tailored to suit the specific risks and needs of the organization, ensuring a more targeted and effective audit process.

Improved Decision-Making: The insights gained from risk-based audits contribute to informed decision-making. Management can use audit findings to make better decisions related to resource allocation, process improvements, and risk mitigation strategies.

Disadvantages of risk-based auditing

As with any approach, there are also some “gotchas” to be aware of; these include:

Inherent Subjectivity: Risk assessment and prioritization involve a degree of subjectivity, and different individuals may perceive risks differently. Inconsistencies in risk identification and assessment may lead to challenges in developing a universally accepted risk profile.

Resource Intensive: Implementing a risk-based audit approach can be resource-intensive, especially in terms of time and personnel. Smaller organizations may struggle to allocate sufficient resources, potentially resulting in incomplete or less effective risk-based audits.

Complexity in Risk Measurement: Measuring the magnitude and impact of risks can be complex, particularly when dealing with intangible or emerging risks. Difficulty in quantifying risks may hinder the ability to prioritize effectively and allocate resources appropriately.

Overemphasis on High-Risk Areas: Excessive focus on high-risk areas may lead to neglect of lower-risk but still important aspects of the organization. Neglecting moderate or low-risk areas may result in missed opportunities for improvement or identification of potential issues.

Limited Historical Data for Emerging Risks: Emerging risks may not have sufficient historical data for accurate assessment. Organizations may struggle to identify and address risks that are novel or evolving, potentially leading to delayed responses.

Complex Communication of Risks: Communicating complex risk information to stakeholders can be challenging. Miscommunication or lack of clarity may lead to misunderstandings among stakeholders, affecting their perception of the organization’s risk management capabilities.

Summary

Risk-based auditing is a strategic approach in quality management that prioritizes audit efforts based on critical risks. It aligns with organizational objectives, optimizing resources and fostering a proactive risk management culture. The method involves risk assessment, tailored audit planning, and continuous improvement. Benefits include resource optimization, strategic alignment, and enhanced stakeholder confidence.

Key Follow-Up Activities:

- Implementation of Risk Mitigation Strategies:

- Continuous Workforce Engagement:

- Monitoring and Evaluation:

- Documentation Review and Update:

- Feedback Mechanism Enhancement:

By actively pursuing these follow-up activities, the business can ensure the sustained effectiveness of risk-based auditing, fostering a resilient and continuously improving organizational environment.